Make in India for jobs and growth – Can Modi deliver the promise?

“More than anytime in history, mankind faces crossroads. One path leads to despair and utter hopelessness, the other to total destruction. Let us pray that we have the wisdom to choose correctly” – Woody Allen

The US subprime fiasco has forced US and European central banks to open their liquidity floodgates and subsequent 50 bps rate cut by US Fed was so called “corrective measures” to contain damage to aggregate demand. The market is also expecting couple of more rate cuts in coming months so as to prevent already slowing US economy from going into recession. However other central banks are still hawkish or neutral with the main policy objective of fighting inflation and its expectation. This un-alignment of interest rate outlook has resulted in so called “structural decline” in US Dollar against the most of the world currencies particularly Euro and emerging markets (EM) currencies. Equity markets all over the world (more particularly EM equities) are rejoicing these dynamics as it is “obvious” that the capital will flow from growth scare region (US) to growth abundant regions (EM like China and India). “Soft landing” in US seems the most likely scenario as despite significant housing market weaknesses, the other pillars of US economy like job market and US consumers are still resilient and, dollar weakness coupled with strong demand from overseas is helping US exporters and MNCs in the need of hour. The “De-coupling” thesis, according to which the world growth is no more depend significantly on US consumption, is more prevalent if not the “Re-coupling” thesis, according to which the US and European Union (EU) growth is now well supported by growth in the rest of world particularly EM economies. And the “Growth Expectation” of emerging markets are well supported by their internal dynamics as their population (India + China accounts for +40% of world population) aspire to consume more goods and services in line with their developed counterparts thus fueling growth.

Seems perfect balancing acts then look at some of the imbalances.

The magnitude of “US consume and EM produce” arrangement based on labor arbitrage, resulting in the transfer of the world’s savings (current account surpluses) to US (twin deficit – current account and fiscal), is unprecedented in recent times and probably cannot sustain indefinitely. If it ends structurally and gradually (as expected by markets) by moving exchange rates and interest rates in a direction that will lead a decline in this imbalance (i.e. lower US dollar and higher US interest rate) it is fine. But it does not seem to be a case as of now. US interest rates are headed lower after monetary tightening of last few years and though US dollar is declining structurally against Euro and EM currencies, EM economies (like India) does not seems to be in a favor of further strengthening of their currencies. “US consumers” has so far consumed beyond their means supported by wealth effects (appreciating housing prices and equity markets over a period) but not by any savings and income growth. With housing prices in US now correcting there will be need to save more due to negative wealth effects which will eventually take its toll to US consumption, the main driver of the world growth so far. Though consumption levels are increasing among EM economies, they are still not sufficient to offset a structural decline in US consumption. “Liquidity glut” induce by central banks lead by US Fed after the burst of tech bubble has fueled “Asset Inflation” all over with hard commodities, crude oil, EM equities and EM housing quoting at multi year high though entire rise can not alone attributed to liquidity glut (Some fundamentals are also at play like strong growth of EM, EM investment binge, demand-supply mismatch, dollar decline, etc). “Inflation scare” has also emerged in soft agro commodities with many agro commodities are significantly high on y-o-y basis. With inflation scare still looming, EM central banks can not afford a loose monetary policy and will have inflation and liquidity controls a priority over a blanket growth policy. With direct and in-direct exports still a significant part of EM economies and their growth, large scale liquidity invasion fueling asset inflation and currency appreciation of EM is not desirable by many policy makers. With many new capacities coming in EM directly or indirectly linked to exports or driven by high capacity utilization and prices of commodities, price crash of commodities in wake of US growth scare or slower EM investments might result into unproductive investments and unutilized capacities in years to come. In today’s globalized and better integrated world many such imbalances exits which need to corrected. Better if those imbalances corrects gradually and softly.

So after nearly five fat years, is the global economy headed for trouble? Answers lie in actions (or inactions) of policy makers in times to come. Let us pray that they have the wisdom to choose correctly.

Indian Economy and its near term policy priorities…

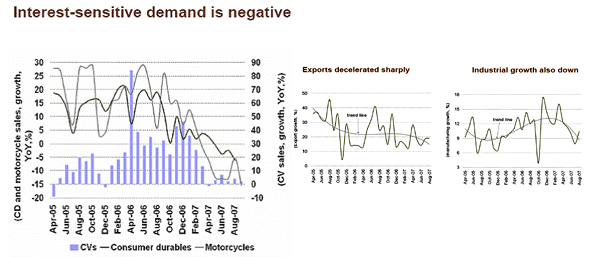

Clear signs of soft landing in the growth cycle… Firm control on overheating

After sustaining strong growth for about nine quarters, there are clear signs that the growth trend is moderating. Growth in demand for commercial vehicles, consumer durables and two wheelers is clearly trending down. High property prices and sharp rise in lending rates has led to slow down in mortgage credit demand. If one adjusts for the 15% y-o-y rise in property prices, real estate volumes are down by 20-25% y-o-y. Exports growth in rupee terms has also slowed to an average of 7.2% in the six months ending June 2007 from 18.3% during QE-December 2006.

Liquidity situation is very easy…

Y-o-y credit growth has come down from 27-31% range in Oct’06-Feb’07 period to ~ 21% in recent months whereas y-o-y growth in deposits is still hovering around 25%. This has resulted in an incremental Loan to Deposit ratio to plunge from ~ 100% in last three years to 45% recently whereas deposit rates are higher by 250-300 at present.

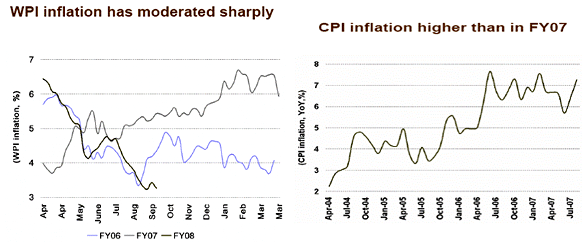

Slowing credit growth (mainly on consumption side), higher deposit growth and easy liquidity conditions clearly warrants an easy monetary policy by RBI to boost credit demand. However, credit growth is likely to be strong from investment side as the recent capital control by RBI for overseas borrowing for domestic us by corporate will force companies to borrow from domestic markets. And though WPI has come within comfort zone of RBI, CPI is still running high. Strong capital flows from overseas are also creating some discomfort for RBI as resultant rupee appreciation and liquidity glut have made things more complex for RBI. These factors are likely to prevent RBI for easing monetary policy as of now instead we expect RBI to give priorities to currency and liquidity management with commitment to maintain control over inflation.

In a situation when structural decline of dollar is inevitable, why Indian policy maker are wary of further rupee appreciation? Logic is simple. Over last five to six years, exports have emerged as a critical driver of the economy. Incrementally it has contributed 25-30% of the growth. Particularly in manufacturing sector, exports have contributed more than 50% of growth. Recent sharp appreciation of rupee and moderation in US growth has already started affecting India’s exports particularly on manufacturing side. The employment intensive SME sector is likely to be affected the most and if policy makers do not act to arresting rising rupee, it might have social and political ramifications.

In a situation when huge investments is required in India’s infrastructure and new capacities, why Indian policy maker are wary of steep rise in capital flows? Again logic is simple. Indian economy is not mature enough to handle it too soon too fast. With US slowdown and declining dollar, it is obvious to see a shift in assets away from US to EM. But is EM has sufficient appetite to absorb this shift without causing significant asset inflation or currency appreciation? Answer is no. For example, 1% shift in equity portfolio away from US to emerging markets will results in capital flow of ~ USD 190 billion to EM and USD 20-25 billion to India. It can push NIFTY up by 2,000-2,500 points. A 50% rise from current levels. No policy makers can ignore such kind asset inflation as such kind of asset inflation might put entire economy at risk? Risk definitely not worth taking

Near term policy expectations

- RBI is likely to maintain status quo on lending rates and it may increase cash reserve ratio by 0.25% to 0.50% in its meeting on October end

- RBI is likely to highlight the heighten risk posed by the global economy and current level of Asset inflation

- Concerns for slower credit off take will be muted because a soft landing is desired by RBI

- RBI is likely to reiterate its commitment to control inflation and will give priorities to currency and liquidity management. It may tighten control on debt related capital flows and may relax criteria for capital outflows

- Indian government may announce some export sops to SME sectors to maintain their export competitiveness affected by recent rupee appreciation

Indian Economy… Where the elephant is headed?

In recent years, the Indian economy has shown remarkable performance with annual growth rate close to 9%. India’s reputation as a destination for outsourcing services in yesteryears has been replaced now with an Economy with full of potential. Expectations are that in several decades it will be world’s third largest economy after US and China. India has sufficient structural dynamics in place to sustain its economic growth. Positive demographic profile, Entrepreneurial cultural, resilient economy, vast resource base, large labor markets, lower level of living standards are some of the structural dynamics that will keep on driving India’s economy. Also on demand side, Indian markets offers a tremendous potential as spending power and growing aspiration of its consumers will increase India’s consumptions to many times from current level. May be India along with China may become what was US today -Central stage of the global economy. But wait, that can’t happen too soon too fast. Mantra of the success is steady rise, sustainable rise and structural rise. May be the elephant way

Is annual growth around 9% sustainable… Only till global cyclical tide is on

Structural growth v/s cyclical growth: Out of India’s current annual growth of ~ 9%, at least 2-3% growth can be attributed to global economic cyclicality so the structural growth rate of Indian economy is currently at 6-7%. With longer term structural dollar decline in place, we should take at least 1% off from India’s structural growth rate. This gives us a sustainable structural growth rate of Indian economy at 5-6% when global cyclical tides turn away. We expect global cyclical tides which has lifted all the boats (from exporters to commodity producers) to turn by 2009 if not in 2008. To attain much higher level (8-9%)of structural and sustainable growth in absence of cyclical growth, Indian and its policy makers need to address many structural challenges and to overcome those challenges. Key challenges for Indian policy makers are to make growth more inclusive, boost agricultural output, upgrade physical infrastructure, labor market reforms, consolidation of public finance, reducing red tape and corruption. Based on realistic assumption that many of the country’s structural problems may not be fully resolved, we expect Indian Economy to cool down from current 9% annual growth level (which may sustain further for a year or two) to around 6-7% annual growth in next decade. This is also a desirable outcome as supply side constrains might put significant pressures on Inflation if growth does not cool down which might eventually lead to a hard lending. Caveat Emptor: Global imbalances discussed at the start of this article need to be corrected. It will be better if they corrects gradually. In case of any sharp corrections in those global imbalances might lead a hard landing in many parts of the global economy and in case of such adverse shock scenario, India might see some downward blips in our already cool downed growth expectations.

Despite the structural challenges India is facing to attain higher level of structural growth, India has tremendous upward potential. The elephant has awaken and moving slowly and steadily. No issue as it is rightly said “Slow and steady wins the race”.

by Manish Marwah